I have been talking about the way things are shifting on this planet. There used to be first world countries, and what were politely called developing countries. Nowadays, there is the Failing West, and the Global South, most of which isn’t in the south at all.

The Global South is going places. The West is sliding backwards. If you are interested in real estate that is something worth taking notice of.

I cover this aspect of the housing market in my book The Ultimate Real Estate Guide, which is now in its third edition. I’m taking most of the information in this blog from that book.

There are various ways of looking at valuations. I recently did a valuation of a small apartment. The seller wanted €60,000 for the place. She’d previously bought it for €90,000. I valued it at €35,000. Each valuation had its validity, but which one was the right one?

In order to answer that question we need to delve into the whole business of how it is that houses get to be the price they are, and what events affect the prices, making them go up or down.

There are several things we need to look at. First, we need to put the whole housing market into some kind of context within society. Some homes are tents surrounded by goats or sheep. The valuation of that family unit is based upon the number of animals, and the amount of land the family has at its disposal for food for the flock. If the animals are healthy then they obviously have enough to eat, and so the land is sufficient. The value of the unit is therefore determined simply by the size of the flock.

In a feudal society things are much the same. The villagers don’t own anything. The lord of the manor owns the lot, and his worth is counted by how many villagers he has. There is an amusing story about such a valuation in nineteenth century Russia called Dead Souls.

You don’t get away from that model until the rise of the merchant class, and the eventual expansion of that class into a proper middle class. Things then become valued in terms of the money they produce. That model changes again when the working class starts to earn enough money to have a disposable income instead of just a subsistence wage. The model changes yet again once sophisticated financial systems develop, in particular, mortgages.

Let’s build on this and see how we can use these ideas to construct a reasonable assumption about how house prices are likely to behave across an updated view of the world.

Let me first take the example I give in Chapter 6 of The Ultimate Real Estate Guide. I take a look at what happened as the UK grew out of the industrial revolution. We can then transpose those developments onto the newly emergent economies in the Global South. You will then be able to see where the future opportunities are.

We need to understand that the main driver of house prices is the availability of money. There are all sorts of silly ideas about what drives house prices, 99% of those ideas are fancy garbage. You need to concentrate on the money.

The average wage of someone in the Victorian era was less than £1 a week. You can’t save to buy a house on that kind of income, and there weren't any mortgages out there. Mortgages in those days were loans, and you either paid back the loan within the stipulated time at the stipulated rate, or you lost the property. Literature of the eighteenth and nineteenth centuries abounds with stories based around people who mortgaged their family homes and wasted the money gambling. There are also stories galore of large estates going to wrack and ruin because their owners could not afford to maintain them.

I note that the Sherlock Holmes stories contain several mysteries which centre around houses that are falling apart. Of course, in Conan Doyle's time, at the end of the Victorian era, property was generally regarded as a liability.

The first change in centuries came after the first world war. At this time there was a new mood in the country. Universal education was beginning to have an effect, and the UK was beginning to change its whole social and fiscal fabric. Wages were rising, and industrialisation gained impetus not only from the war effort and post-war regeneration, but for the first time ever the peasantry were not on subsistence wages.

However, all was not rosy, and the thirties was a grim time, closely followed by another horrific war.

It wasn't until the mid fifties that things began to gradually improve. There was still rationing in 1951.

From 1956 onwards a real working class with some spare cash started to emerge, and the middle classes started to recover from forty years of stagnation. At that point house prices were on the floor. Adjusted for inflation, house prices in the UK were no higher than in 1760.

Let’s analyse what happened from 1956 onwards in the UK, and see if we can draw any conclusions as to what affects house prices, and whether we can transfer those conclusions to the newly emerging economies.

Several things have made house ownership fashionable. First, people in the fifties had an ingrained desire to own their own homes. Home ownership was a working class dream.

Second, people started to get what was, historically speaking, massive wage rises. Prime minister Macmillan was always bleating that "you've never had it so good". Pay rises were running at twice the rate of inflation. It was unheard of.

If you have the money, you'll spend it. For the first time ever, large swathes of the population could realistically look forward to owning their own home.

By 1970 the second important necessity for the expansion of home ownership was in place: namely, sophisticated mortgages. Until you could get a 90% mortgage, very few people had enough money to put down a deposit for the purchase of a house. Once that barrier was breached the floodgates were open. It didn't take long before 100% mortgages became available, and then everyone with a half decent pay packet could buy a house.

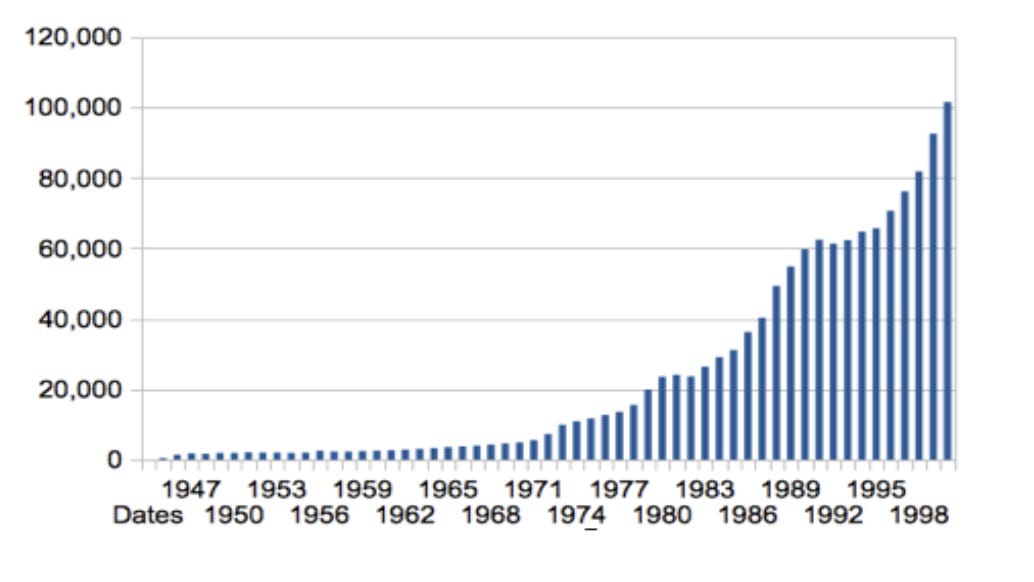

So, property prices did nothing for centuries because very few people had the money to buy. Once the money was there, people started buying. Purchase was then facilitated by two things. First, the entry barrier to getting a mortgage was lowered, and subsequently almost entirely removed. Secondly, wages rose faster than inflation thus giving households a disposable income. And here’s a chart to prove it.

We must remember that the term "disposable income" couldn't be applied to 90% of the population before 1918. The percentage didn't rise significantly until after 1956.

Now look at the house price charts, and see where house prices started to move up. It's obvious. Give people the money and the financial instruments and they will go out and buy. Without them they will not.

I will take this argument a lot further next week, and see how we can apply these principles to the newly rich countries. And eventually show you how you can take advantage of what is coming to improve your own wealth just at the time your existing wealth is about to be sabotaged. See you then.

The Ultimate Real Estate Guide can be bought from Amazon. Here is the UK link:

https://www.amazon.co.uk/dp/B07D3ZW8D2

The US link is only slightly different: https://www.amazon.com/dp/B07D3ZW8D2

Share this post