As stated in my previous blog I am looking for investments in a chaotic world. My first love is real estate, so I shall be looking in that direction first.

What is the most influential driver in the real estate markets? That is an easy question to answer. Basically there is one great influencer when it comes to houses; the cost of money. There are other factors to look into, but compared with the cost of money, they are almost incidental.

Anything that distorts the cost of money affects the price of houses.

People claim that house prices always go up, which is nonsense. Generally speaking house prices mirror the value of the local currency. If that currency starts to fall, house prices tend to rise to counter that fall.

If the government starts to interfere with the natural house price market that will also affect prices, usually for the worse. People who cant normally afford to buy are encouraged to buy through artificially massaged loans, which under normal circumstances those taking the deals cant afford, and so they are encouraged to destabilise their ability to cope, which in turns starts to destabilise the rest of the market.

The government also directly causes house prices to crash. It happens in a way that is staring us in the face right now across most of the western world. Let me walk you through how it happens.

Governments are notoriously bad at budgeting. They spend far more than they take in through taxation. To pay for the deficit they issue bonds which are sold to the public, and those bonds carry what is called a coupon, which is the level of interest they pay. To make sure people and organisations buy the bonds they have to compete in the market place for buyers, which means they have to pay the going rate in interest to the buyers (lenders). The more dodgy the government’s financial position, the higher the interest rate needs to be to attract those buyers.

There is a rather interesting indicator which tells the public whether these bonds are good in terms of security.

This is the point where I ought to present a simple, obvious, but usually ignored general rule about borrowing.

Sensible people (and governments should come into that category but rarely do) only borrow under certain auspicious terms.

There is a golden rule that before you decide whether to borrow money, you need to ask yourself what it is you are borrowing for. Governments should be borrowing to achieve an end. That borrowing can be represented by a simple equation which can start out as a simple text description. It should then be possible to convert the text to an algebraic equation. The golden rule is that any such equation should end with an equals sign followed by a positive number. If =x comes out with x being a negative number, then the operation which is proposed is going to lose money and should not even be considered.

When applied to governments there is an index which shows that when a certain debt level is reached any further borrowing is likely to create a bigger debt situation. There comes a point where a government borrows to lose money because the cost of the interest on the debt erases any value in what otherwise might be a productive outcome.

There is a general figure at which further government borrowing can never produce a positive figure. That point is reached when the general level of borrowing reaches 90% of the value of the country’s economy. The further above that figure is the level of the country’s debt, the worse the situation is, and a country starts to sink into what is called a debt trap from which it is very difficult to escape.

Usually a government can borrow at advantageous rates if its debt level is well below 90% of the country’s notional economic value, but once it passes that magic level, a country has to offer higher and higher interest levels on further debt in order to encourage buyers to buy that debt.

Obviously the further the debt level increases the more difficult it is for a government to borrow on the open market as interest levels start to become onerous, pushing repayment promises into fantasy land. At this point two things happen. First, commercial interest rates, which follow the government base rate start to rise, and begin to adversely affect business transactions, which tends to slow an economy, and put pressure on other financial deals which, at a lower rate, were performing well enough, but which, at the higher rate, start to wreck profitability, and ultimately send an economy into recession, and bank lending dries up.

When interest rates become punitive a government can only raise money by printing it. Printing money depreciates the existing supply, and we get what is laughingly called inflation, but which is not true inflation, but devaluation.

What you now have is expensive money. Most house purchases are made with borrowed money. Raise the cost of that money and you raise the cost of the house, and make houses less and less affordable.

The result? House prices start to fall.

That is the position we are in right the way across the western world.

House prices are going to start falling. Now is not the time to invest in real estate.

You dont need to guess the future. The sensible person simply does the necessary calculations.

There may well be variations in the way this indicator works, but I will deal with that next week. In the meantime here are the facts. You dont invest in a country where that country is in a debt trap. At 90% the country is entering the danger zone. The higher that figure the more dangerous that country is economically speaking, and the less attractive the country is to invest in, so dont.

Here’s a small list of a few of the worst countries to invest in:

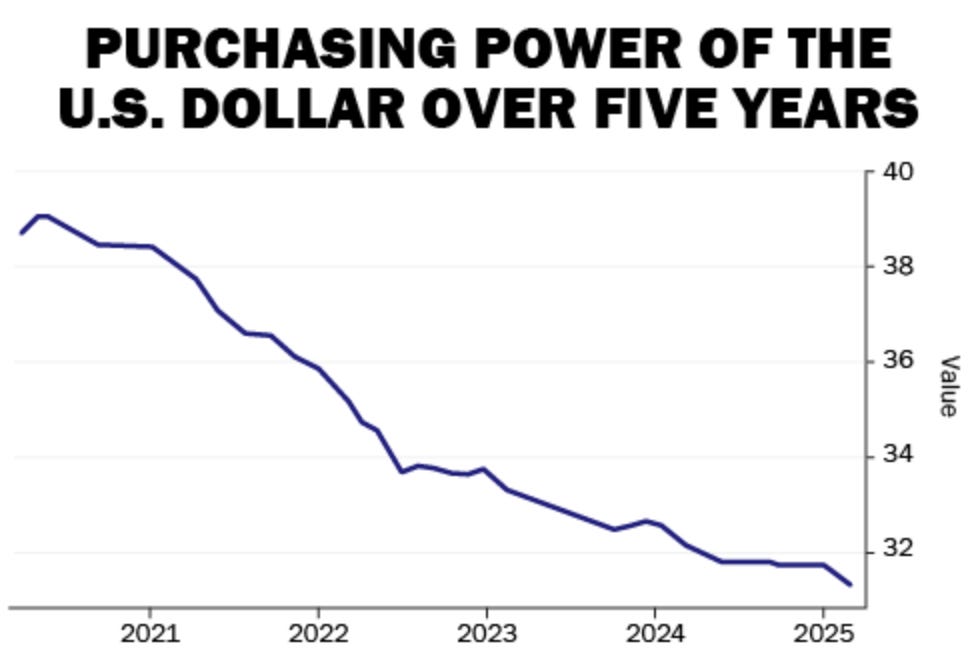

And to show you what happens when a country starts printing money, just look at how the US dollar is tanking over the years. Clearly, investing in a dollar denominated currency is not a good idea at all. Clearly the sensible person does not invest in a falling currency

Hmmm…. Does this mean we need to start looking at BRICS+ currencies? In a later blog I will investigate that possibility. Next week I will also look at another indicator.

Share this post